DFW Builder Incentives Explained: New Construction Homes With Rates Under 4%

If you have been waiting for the right moment to jump into the market, the current round of DFW builder incentives might be the thing that finally gets your attention. Builders across North Texas have already been doing the usual playbook for a while now: closing cost help, price cuts, and rate buydowns. That part is not new.

What is new is this: one builder is offering select interest rate options under 4% on inventory homes, and that is not something I have seen much of lately. If you are buying new construction in DFW, these are exactly the kinds of deals worth paying attention to because they can change the monthly payment enough to make a home feel realistic again.

There is a catch, and I will get into that. But there is also real opportunity here, especially if you are flexible on community, floor plan, or timing.

Table of Contents

- Why DFW Builder Incentives Are Increasing

- DFW Builder Incentives With Rates Under 4%

- What A 5 Year ARM Actually Means

- Home 1: Pilot Point New Construction Under $420K

- Home 2: Rockwall New Construction Near $665K

- Home 3: Melissa New Construction Under $500K

- Home 4: Rockwall New Construction Near $700K

- What DFW Builder Incentives Mean for Buyers

- How to Maximize DFW Builder Incentives

- FAQs About DFW Builder Incentives

- Final Thoughts on DFW Builder Incentives

Why DFW Builder Incentives Are Increasing

The short version is simple. Builders need to move homes.

When a builder has standing inventory that has been sitting too long, they start looking for a different lever to pull. Sometimes they have already reduced the price as much as they want to. Sometimes they are carrying those homes longer than planned and the holding costs start adding up. At that point, a big incentive package can make more sense than another obvious price drop.

That is why DFW builder incentives have become such a huge part of the conversation. Instead of only advertising a lower sticker price, builders are using financing to make the home feel more affordable month to month.

And if you are buying new construction in DFW, monthly payment is usually what decides whether a home works or does not.

What is interesting right now is that some builders are reportedly spending somewhere around 6% to 9% per transaction on things like closing costs and rate buydowns. That is real money. It also tells you they are serious about getting inventory sold.

VIEW NEW CONSTRUCTION DEALS IN DFW

DFW Builder Incentives With Rates Under 4%

Most builders lately have been offering pretty standard financing incentives:

- Help with closing costs

- One year or two year temporary rate buydowns

- Price reductions on quick move in homes

- Occasional three year buy down structures

The unusual part here is that this builder had multiple financing options that dipped below 4%, including:

- 3.75% FHA on select homes

- 3.99% conventional on select homes

- Alternative fixed options in the mid 4% to low 5% range depending on the loan type and program

These offers were tied to certain inventory homes in places like Pilot Point, Rockwall , and Melissa . Not every home qualifies, and not every rate structure is identical, but the point stands: some of the best DFW builder incentives right now are showing up in financing, not just in headline pricing.

What A 5 Year ARM Actually Means

Before anybody gets too excited, let’s talk about the part that needs real caution.

One of the options being offered is a 5 year ARM, which means adjustable rate mortgage. In this case, the rate stays fixed for the first five years. After that, it can start adjusting based on market conditions.

The way this was explained is that the adjustment would not immediately jump from a low teaser rate straight to whatever the market is doing. Instead, it would step up gradually, with limits on how much it can increase year over year. That still does not mean you should take it lightly.

A 5 year ARM can make sense if:

- You expect to sell before the fixed period ends

- You believe you will refinance before the adjustment period matters

- You need the lower initial payment to make the numbers work today

- You fully understand the risk if rates stay high or go higher

A 5 year ARM probably does not make sense if:

- You are stretching just to afford the home now

- You plan to stay long term and cannot comfortably handle a higher payment later

- You are assuming refinancing will definitely be available on favorable terms

This is where a lender has to run the actual scenario with you. One of the biggest mistakes people make with DFW builder incentives is treating the advertised rate as the full story. It is not. The structure matters just as much as the number.

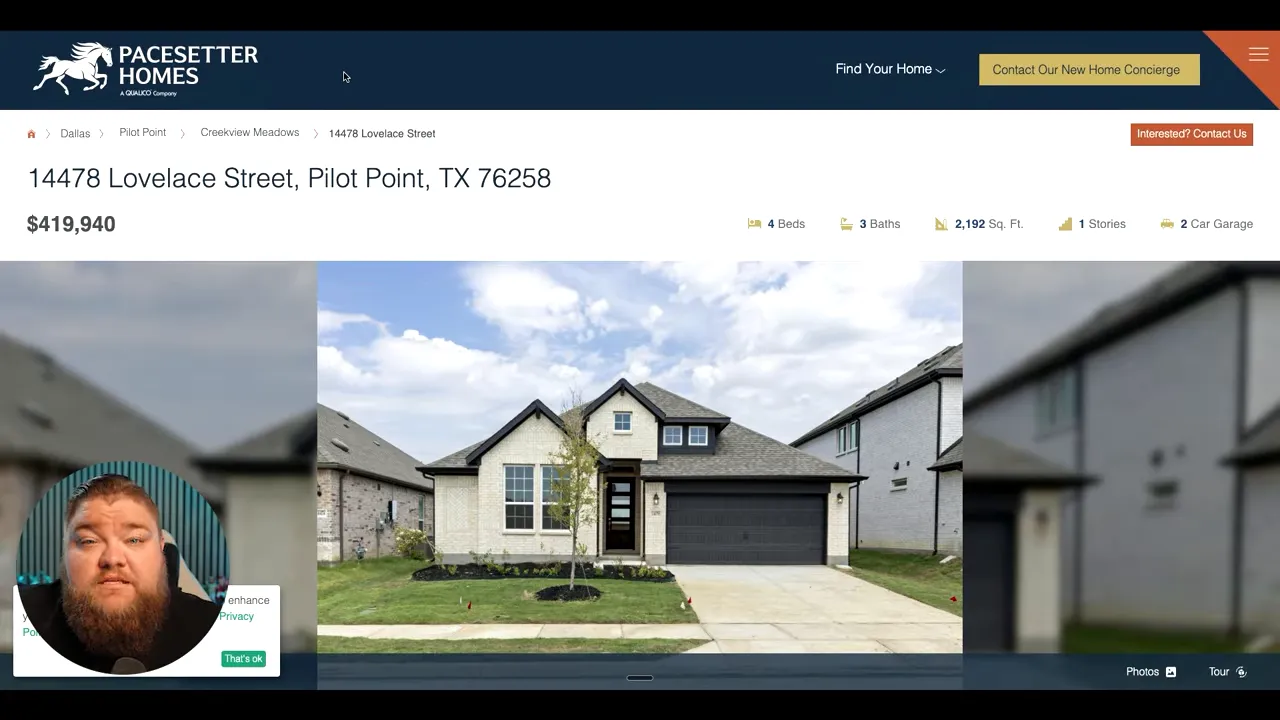

Home 1: Pilot Point New Construction Under $420K

The first example is in Pilot Point, in Creekview Meadows.

This home was listed around $419,940 and offered one of the lower financing options available. The basic setup looked like this:

- 4 bedrooms

- 3 bathrooms

- Just under 2,200 square feet

- Covered patio extension

- Front secondary bedrooms plus study layout

- Primary suite at the rear of the home

On the financing side, the example used:

- FHA loan

- 3.5% down

- 3.75% rate

- Estimated insurance around $1,900 annually

- Estimated property tax rate around 2.5%

Using those assumptions, the principal and interest landed at roughly $1,905 per month. Once taxes, insurance, and mortgage insurance were added, the total monthly payment climbed from there, but the key takeaway was the starting point. That principal and interest number is dramatically different than what a buyer would see at a much higher conventional market rate.

That is the power of strong DFW builder incentives. They may not magically erase taxes, insurance, or FHA mortgage insurance, but they can lower the monthly cost enough to reopen neighborhoods that previously felt out of reach.

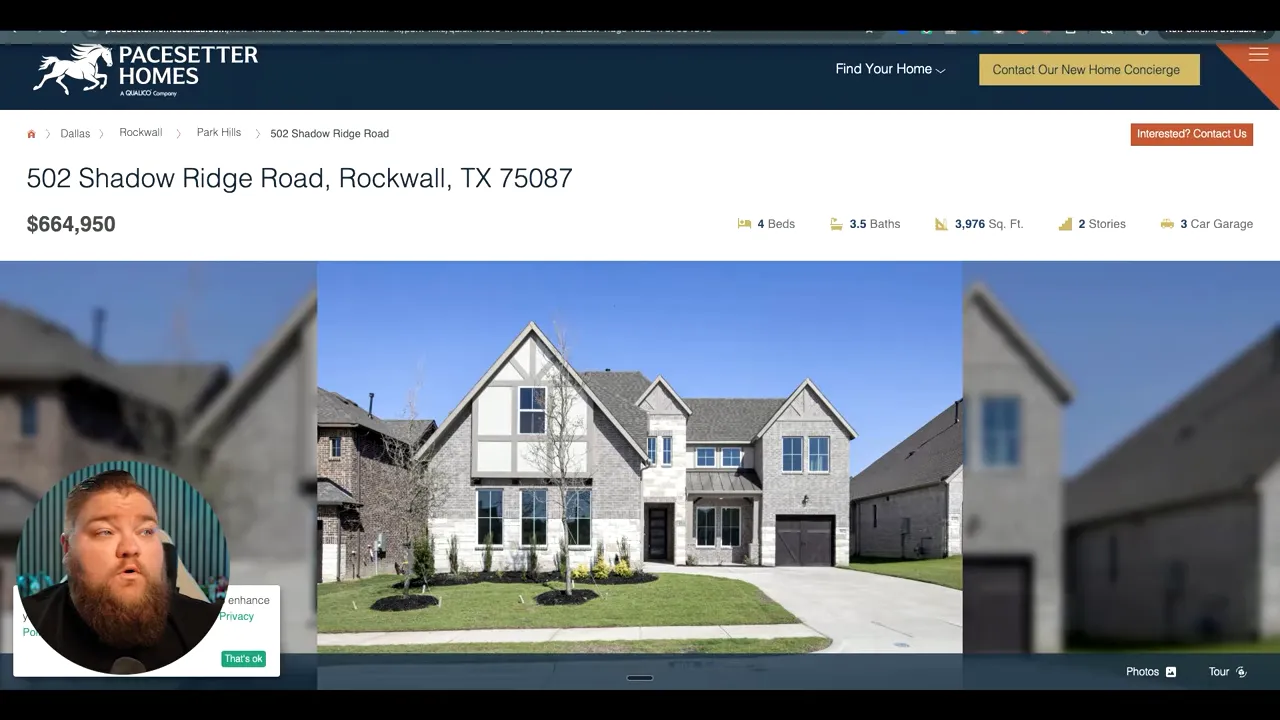

Home 2: Rockwall New Construction Near $665K

The next home jumps way up in size and price point, but it is a great example of how incentives matter even more on larger homes.

This one was in Rockwall, priced around $664,950, and it was one of the larger floor plans from Pacesetter Homes. If you are not familiar with Pacesetter, they sit in a nice middle ground for a lot of buyers. They are not a tiny custom operation, but they are also not pumping out homes on the scale of the biggest production builders.

The home details were strong:

- 4 bedrooms

- 3.5 bathrooms

- Nearly 4,000 square feet

- 3 car J-swing garage

- Study downstairs

- Large kitchen and dining area

- Game room upstairs

- Media room included

The neighborhood also had something buyers are constantly asking for: low taxes. The estimated tax rate here was around 1.52%, with no MUD and no PID. That matters a lot in DFW, where tax burdens can quietly wreck what otherwise looks like a manageable payment.

The sample payment used these assumptions:

- Conventional loan

- 10% down

- 3.99% rate

- Insurance estimate around $1,900 annually

- Tax rate estimate of 1.52%

That put principal and interest at roughly $2,800 per month, with taxes, insurance, and PMI added on top.

For a home pushing 4,000 square feet in Rockwall, that is exactly why buyers need to pay attention to DFW builder incentives. A single percentage point on a loan this size is a huge swing in monthly payment.

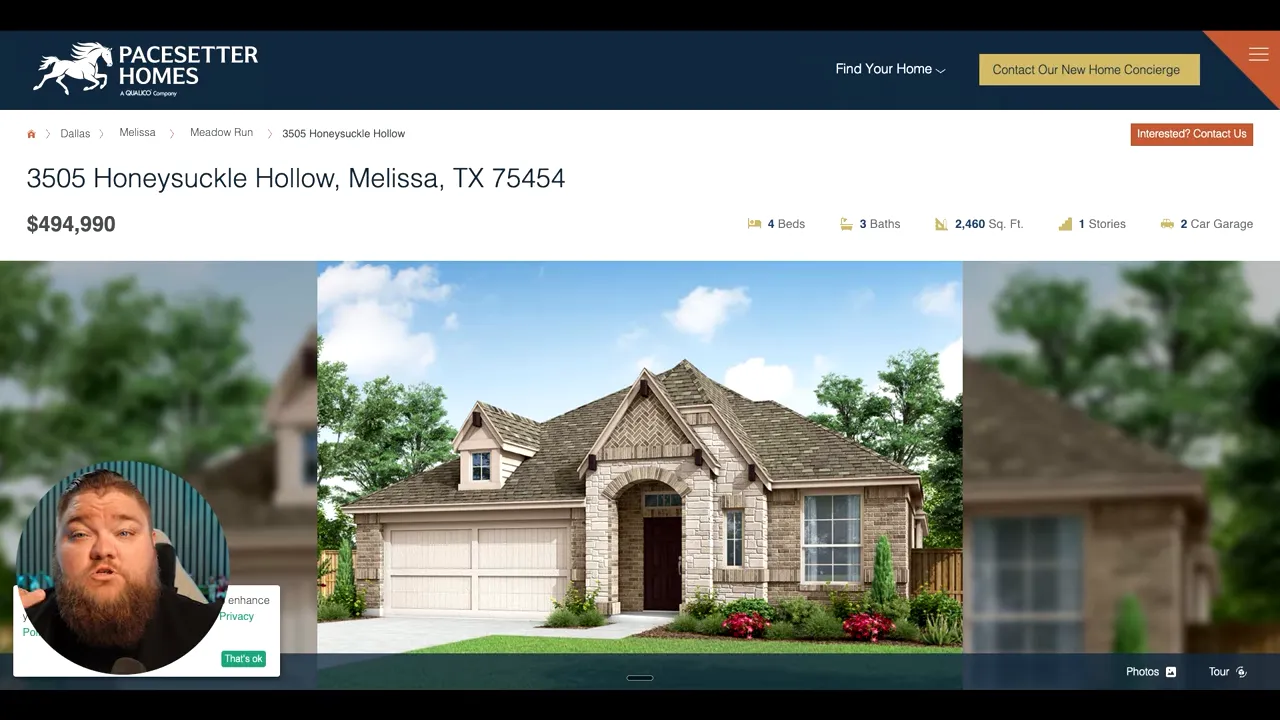

Home 3: Melissa New Construction Under $500K

Melissa continues to be one of the more interesting pockets north of Dallas, especially for people who want solid schools, a family oriented environment, and room to grow without landing in the middle of the craziest price points.

This example was an Addison II floor plan in Melissa priced around $494,900.

Here is what stood out:

- 4 bedrooms

- 3 bathrooms

- About 2,460 square feet

- Study space

- Game room positioned between secondary bedrooms

- Large family room layout

The community itself was another key part of the story. It is not one of those giant master planned neighborhoods with a mountain of amenities and a giant HOA bill attached. Instead, it is a smaller community located near Melissa schools, including the high school and middle school, with an elementary nearby as well.

And once again, taxes were a selling point. This neighborhood had:

- No MUD

- No PID

- Tax rate around 1.901%

The sample payment for this one used a 4.25% conventional rate and estimated total monthly payment at around $3,294, with principal and interest in the neighborhood of $2,187 before the rest of the carrying costs were added.

For anyone buying new construction in DFW, Melissa deserves more attention than it gets. It is one of those spots where the numbers can still feel livable if you catch the right house with the right financing package.

Home 4: Rockwall New Construction Near $700K

The last example circled back to Rockwall, this time at around $699,900.

This home checked a lot of boxes for move up buyers:

- About 3,500 square feet

- 4 bedrooms

- 3 bathrooms

- 3 car J-swing garage

- Media room

- Close to schools, including a nearby freshman center and walkable elementary access

The neighborhood was again a smaller scale community with lighter amenities, but that tradeoff helped keep the tax burden attractive. The estimated total tax rate here was around 1.56%.

The payment example used:

- Conventional financing

- 4.25% rate

- 1.56% estimated taxes

The exact total monthly estimate was presented as a rough scenario, not a final quote, but the broader point was clear. Even at a higher purchase price, low taxes paired with strong financing incentives can create a more workable payment than many buyers expect.

What DFW Builder Incentives Mean for Buyers

There are two things happening at once in DFW right now.

First, buyers are still payment sensitive. Maybe more than ever. Price matters, of course, but monthly cost is what stops most people in their tracks.

Second, builders know that. So instead of relying only on list price reductions, they are using DFW builder incentives to solve the payment problem more directly.

That is why the best deals are often found on:

- Inventory homes that have been sitting longer

- Homes in communities with slower absorption

- Select plans builders need to move before the next phase

- Homes tied to preferred lenders with special rate structures

This does not mean every new build is suddenly a bargain. It means the opportunities are specific. You need to know where to look, which homes qualify, and whether the incentive is actually good or just flashy marketing.

VIEW NEW CONSTRUCTION DEALS IN DFW

How to Maximize DFW Builder Incentives

If you are serious about buying new construction in DFW, here is how I would approach these deals.

1. Start With Payment, Not Just Price

A $500,000 home with a low tax rate and builder bought down financing can beat a cheaper house with a higher tax burden and worse loan terms.

2. Ask Whether The Rate Is Temporary Or Fixed

This is huge. A temporary buy down is not the same thing as a 30 year fixed. A 5 year ARM is not the same thing as either of those. The headline rate means nothing without the structure.

3. Check Taxes Before You Get Emotionally Attached

No MUD, no PID, and a lower tax rate can make an enormous difference. Melissa and Rockwall stood out in these examples for exactly that reason.

4. Focus On Inventory Homes

The strongest DFW builder incentives are usually tied to homes that need to move now, not homes you are building from the ground up over the next eight months.

5. Run The Numbers With A Lender

Online estimates are useful for getting in the ballpark. They are not enough for final decision making. PMI, insurance, loan structure, and eligibility can all change the outcome.

6. Do Not Assume More Expensive Means Worse Deal

Sometimes the stronger incentive package is sitting on a higher priced home the builder has been carrying too long. You might find more monthly value there than on a lower priced house with weaker terms.

VIEW NEW CONSTRUCTION DEALS IN DFW

FAQs About DFW Builder Incentives

Are DFW builder incentives better than just negotiating a lower price?

Sometimes yes. If a builder can buy your rate down substantially, the monthly payment improvement may be more valuable than a modest price cut. That said, it depends on how long you plan to keep the loan and whether the lower rate is temporary, fixed, or adjustable.

Is a 5 year ARM a bad idea?

Not automatically. It can work for the right buyer, especially if there is a strong plan to refinance or sell before the adjustment period matters. But it is not something to take casually. You need to understand the future payment risk before using that kind of incentive.

Why do some DFW builder incentives only apply to certain homes?

Because builders usually attach their strongest incentives to standing inventory or homes that have been on the market the longest. They are trying to solve a specific inventory problem, not discount every home in the neighborhood.

What should I compare besides the interest rate?

Look at the full payment, tax rate, HOA dues, mortgage insurance, type of loan, down payment requirement, and whether the rate is fixed or adjustable. Great DFW builder incentives can still be a bad fit if the structure does not align with your timeline or budget.

Are low tax neighborhoods really that important when buying new construction in DFW?

Absolutely. In North Texas, taxes can dramatically affect affordability. A lower rate with no MUD or PID can save hundreds per month compared to a similar home in a higher tax district.

Do these incentives last long?

Usually not. Incentives can change quickly based on inventory levels, lender partnerships, and builder sales pace. The best deals often disappear once the qualifying homes go under contract.

Final Thoughts on DFW Builder Incentives

The biggest thing I would leave you with is this: the market is not handing out easy wins everywhere, but there are pockets of real opportunity. The best DFW builder incentives right now are showing up on specific inventory homes where builders are motivated, creative, and willing to spend serious money to make the deal happen.

If you are on the fence, this is the kind of moment worth running the numbers. Not because every incentive is amazing, but because a few of them actually are. And if you can pair the right builder, the right neighborhood, and the right financing structure, buying new construction in DFW can look a whole lot better than it did even a few months ago.

If you’d like me to point you to the specific DFW builder incentives that match your price range and timeline, let’s talk. Call me at 469-707-9077 or book a meeting here to review options together.

Zak Schmidt

From in-depth property tours and builder reviews to practical how-to guides and community insights, I make navigating the real estate process easy and enjoyable.